The pandemic saga continues, and sadly, some of the more pessimistic scenarios that we outlined in the last Quarterly Bulletin are becoming a reality, and the social consequences are severe. That said, there is scope to imagine a post-Covid future with stronger, greener and more resilient Caribbean economies.

I. Introduction

Governments in the Caribbean region have been relatively successful in flattening the infection curve of the coronavirus in their countries.1 Geographical isolation is a contributing factor, but decisive and determined government action has been effective in reducing community transmission. Many potential deaths have been avoided.

Yet this accomplishment has yet to be compensated with an economic reward. As these countries begin to open their domestic economies, they are still battered by external shocks. This is particularly the case for the tourism-dependent economies that experienced a virtual shutdown of the sector during the second quarter of the year. The natural-resource-based economies are also suffering from the lingering effects of the decline in commodity prices and related external demand.

This second special edition of the IDB Caribbean Quarterly Bulletin provides an update of economic conditions in the region. It also focuses on important evolving issues, including the potential impact of the coronavirus crisis on countries’ balance of payments, and on new data from the IDB on the real-time social effects of the crisis. Key impacts include the following:

-

Economic forecasts for 2020 have worsened substantially. In line with simulations conducted in the last Quarterly Bulletin, the economies most heavily dependent on tourism—The Bahamas and Barbados—could experience double-digit declines in GDP this year, as recently forecast by the International Monetary Fund (IMF). Commodity exporters, with the exception of Guyana, are likely to experience a single-digit decline in GDP this year due to the domestic containment shock and lower prices for key commodities.

-

Balance of payments disequilibria remain a concern. In particular, tourism receipts constitute a very large share of export earnings, leading to the potential for double-digit impacts on the balance of payments. A key unknown is how import demand is evolving in response to the tourism decline and economic shutdown.

-

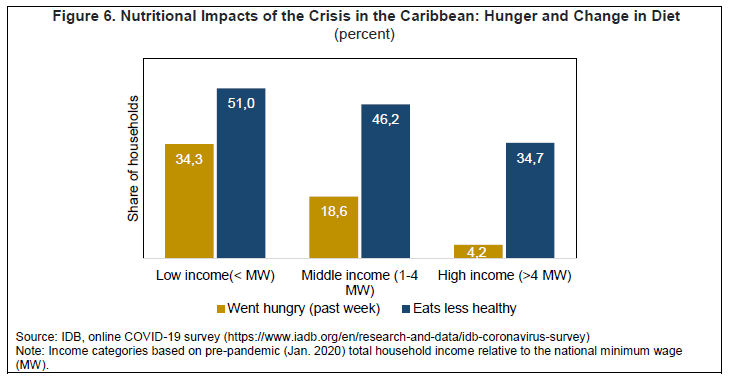

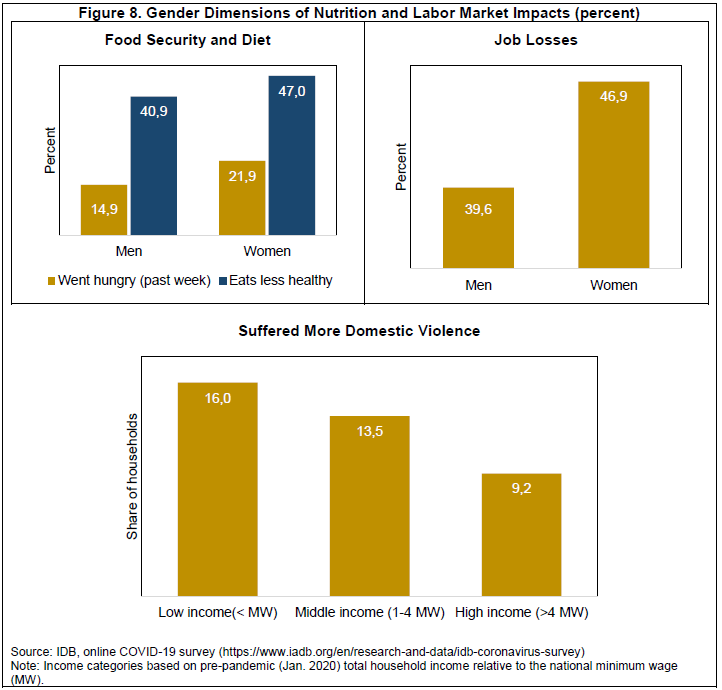

The social impacts of the ongoing crisis are significant. Simulations of the employment impact of tourism shocks provide a sobering perspective. In addition, evidence provided by an online survey carried out in April by the IDB’s Research Department reveal reported household effects.2 For households earning less than the minimum wage, a striking 34.3 percent of respondents declared that they had gone hungry in the previous week, and just over half stated that they had consumed less healthy food. About 60 percent of low-income households reported a job loss in the household. There are important gender dimensions as well: job losses and nutritional outcomes were worse for women, and some women reported an increase in domestic violence.

As is the tradition for this bulletin, the regional overview is followed by country-specific sections that provide more details on recent developments in each of the six Caribbean countries as well as sovereign members of the Organisation of Eastern Caribbean States (OECS).3

II. Progress in “Job 1”: Stopping the spread of the virus

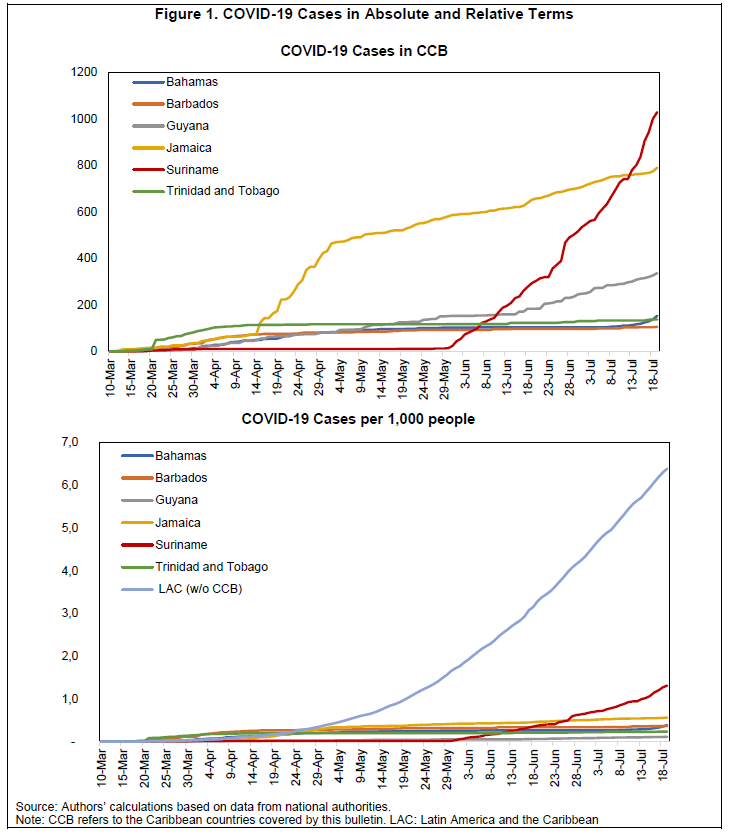

Figure 1 shows that cumulative coronavirus cases have leveled off, albeit at different levels, in five of the six Caribbean countries. The exception is Suriname, where the recent rise in cases followed the May 25th elections, when citizens congregated in the close quarters of polling stations. Prior to the elections, Suriname had gone weeks without any new cases. This case surge is clearly a cautionary tale for countries holding elections during the period when the pandemic persists in a population without universal testing and where cases may be asymptomatic. No country has reached the stage of universal testing. Also, in mid-July, there was a surge of cases in The Bahamas, after the country’s airports were opened to tourism at the start of July. There were also more modest increases in Jamaica and Barbados, since opening the border.

All six countries have deployed international travel restrictions to avoid the arrival of imported cases. Community transmission has been limited through rising levels of testing, quarantines of infected individuals, strong social distancing protocols (including curfews), and effective communications campaigns. Geographic isolation has probably also been a factor. Shutting down airports and ports to all but essential travel, commerce, and the return of nationals from abroad helped to reduce the potential for imported cases to the islands. The continental Caribbean countries—Guyana and Suriname—have dense tropical forest buffers, although there have been reports of infected gold miners crossing the border from Brazil into Guyana and Suriname (through French Guyana).4

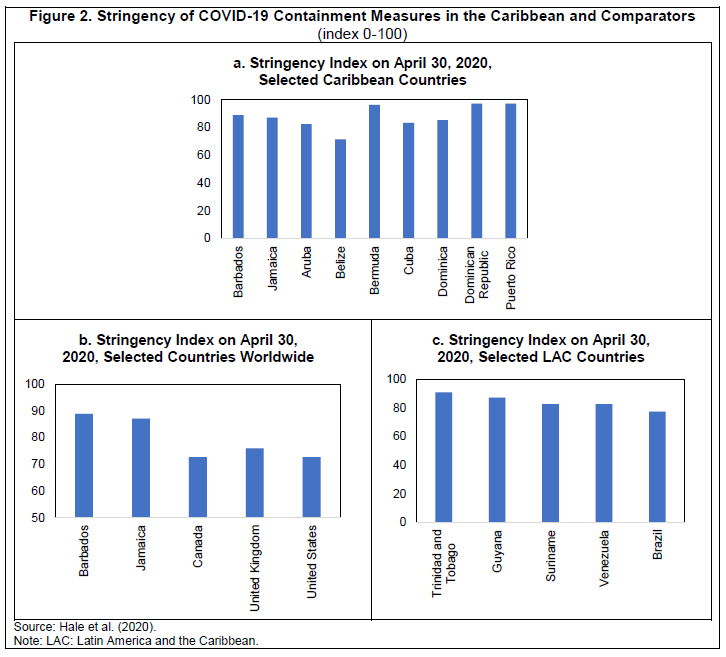

Academic research shows that Caribbean countries have been strong and persistent over time in the stringency of their containment measures (Hale et al. 2020). For example, panel a of Figure 2 shows that while Barbados and Jamaica are about in the middle among competitor tourism destinations in terms of stringency measures, most of the destinations to which they are being compared score quite strongly.5 The data displayed are for April 30, 2020. Panel b shows the risk of opening to tourism from source destinations that have been less stringent in their containment measures. Finally, panel c shows how containment measures compare with neighboring countries in Latin America and the Caribbean.

III. Evolving Economic Prospects

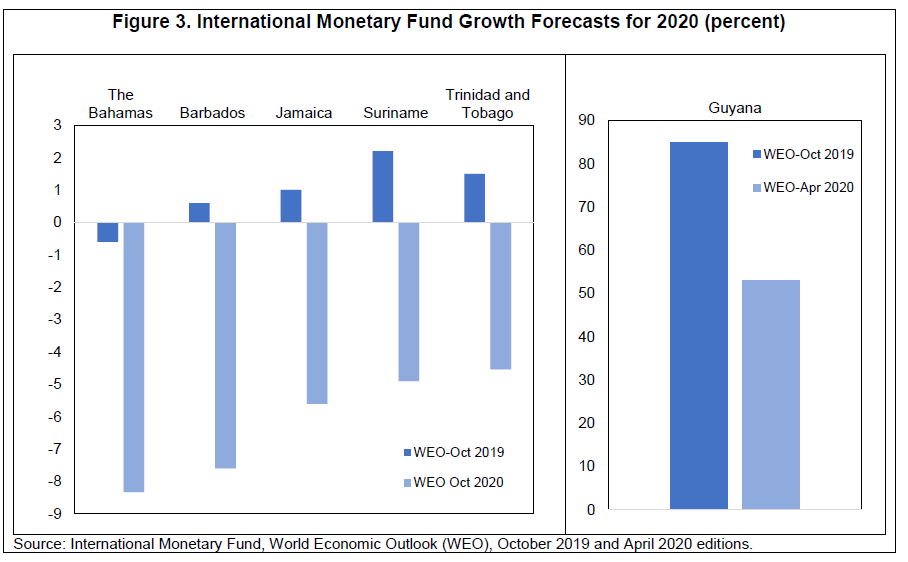

This spring, the IMF revised economic growth forecasts downward for countries across the world, including the Caribbean. This is not surprising given the domestic and external shocks analyzed in the last Caribbean Quarterly Bulletin, which presented simulations showing that the tourism-dependent economies—The Bahamas, Barbados, and Jamaica—could experience double-digit contractions, depending on the assumed depth and duration of the tourism shocks (see also Mooney and Zegarra 2020a). The previous bulletin also outlined the effects of commodity price shocks on Guyana, Suriname, and Trinidad and Tobago, as well as the transmission channels that could lead to a synchronized contraction in the Caribbean.

As an illustration of how quickly and significantly growth assumptions have deteriorated over the past few months, Figure 3 lays out the growth forecasts for 2020 published by the IMF in October 2019, as compared to those published in April 2020 (IMF 2019, 2020a). These forecasts are likely to be further adjusted downward over time. In fact, in the June staff report for The Bahamas’ request for financing under the Fund’s Rapid Financing Instrument (RFI), the IMF further lowered the 2020 growth forecast for that country to -12.5 percent (IMF 2020b). For Barbados, the June IMF staff report for the review of the Extended Fund Facility revised its 2020 growth forecast down to -11.6 percent (IMF 2020c). In brief, the synchronized contraction for 2020 (with the exception of Guyana) appears deeper and more likely.

Caribbean Commodities Exporters

For oil producers in the region, oil prices have recovered somewhat and stabilized at around the US$40 per barrel (WTI), after reaching historic lows.6 This compares to an average WTI price of US$57 per barrel in 2019.7 Future prices set for the next six to 12 months have also stabilized at around US$40 per barrel. That said, there could be substantial volatility because the future evolution of the economies of major oil-consuming countries is highly uncertain, and oil demand is closely linked to economic conditions in those countries. In addition, even with the regained stability of oil prices at present, the drop compared to last year will certainly affect the value of production for Trinidad and Tobago, Suriname, and the new oil exporter, Guyana.

Natural gas prices have continued declining recently, with the Henry Hub price dropping below a new low of US$1.50 MMBtu in late June. Future prices indicate an expected recovery to well over US$2 MMBtu early next year. However, the continued decline of natural gas prices is of concern for Trinidad and Tobago, given that its natural gas production is tenfold larger than its oil production.

Political uncertainty is another issue to monitor in the coming months. The new president of Suriname was inaugurated in mid-July, but the election in Guyana is still under dispute. A recent Caribbean Court of Justice opinion essentially sent the decision-making process back to the Guyanese electoral commission, and at the time of drafting this bulletin, the outcome is not resolved. Elections are scheduled for August 10 in Trinidad and Tobago, and elections will likely occur before the end of the year in Jamaica. Political uncertainty and/or transitions add another challenge for shaping the policy response to the ongoing health and economic crisis.

As noted in the last Quarterly Bulletin, the combination of a domestic shock from required containment measures, along with external shocks, will drive macroeconomic outcomes this year. On the domestic front, partial lockdowns and curfews have succeeded in flattening the curve, as noted above, but they also severely constrained domestic services sectors during the second quarter of this year. Countries are relieving the containment measures leading to a potential upturn in the “face-to-face” services sector.

IV. The Importance of Tourism for Caribbean Economies

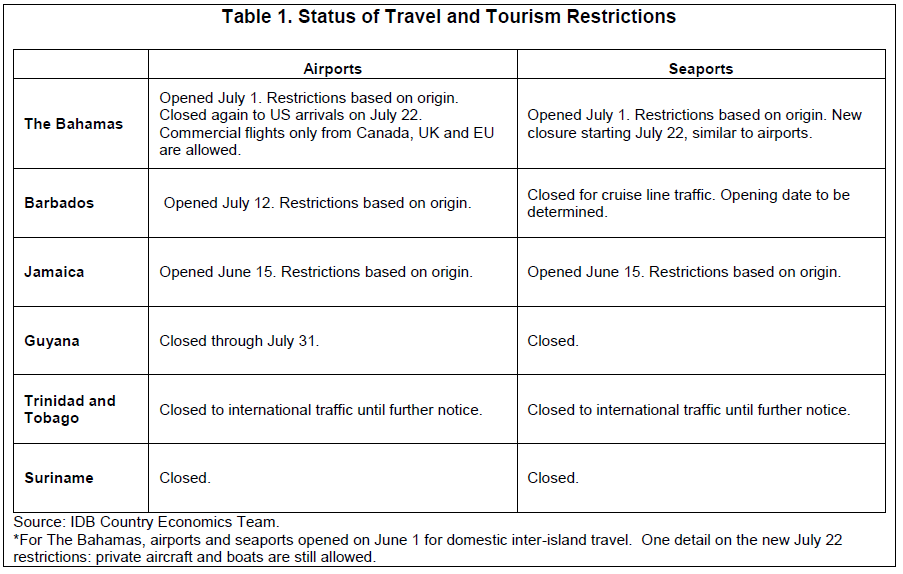

Health protocols are needed to limit the number of imported coronavirus cases, but such protocols prevent tourism access and can dampen demand for tourism and related services. As discussed in greater detail in the individual country sections that follow, countries across the region have now begun to wind down travel and tourism-related restrictions. For example, Jamaica reopened its air and seaports on June 15, but will continue to impose information and screening requirements on travelers, particularly those from high-risk areas. Barbados opened its airport on July 12, and The Bahamas opened its airport on July 1 (Table 1). But these efforts remain in the early stages, and even when points of entry are fully reopened to visitors, it is not clear that all tourism source countries will follow suit in terms of exit and reentry requirements. The risks are real: following a surge in cases in The Bahamas, the government decided to close the country to arrivals from the US where cases are surging. Similarly, demand for tourism will remain constrained for some time owing to concerns about sanitary conditions and because of the economic impact of the crisis on would-be travelers.

Tourism was adversely affected during the first quarter of 2020 as the crisis began to unfold, and the sector was effectively shut down during the second quarter as complete travel prohibitions came into place.8 Expectations for the third quarter remain uncertain, but prospects for a rapid return to pre-crisis levels of demand remain grim. In this context, a recent publication from the IDB Caribbean Department’s economics team—entitled “Extreme Outlier: The Pandemic’s Unprecedented Shock to Tourism in Latin America and the Caribbean”—considers various dimensions of the shock, including dependence of the region’s economies on the tourism sector, as well as the potential impact of the crisis on output, employment, and the balance of payments (Mooney and Zegarra 2020b).9

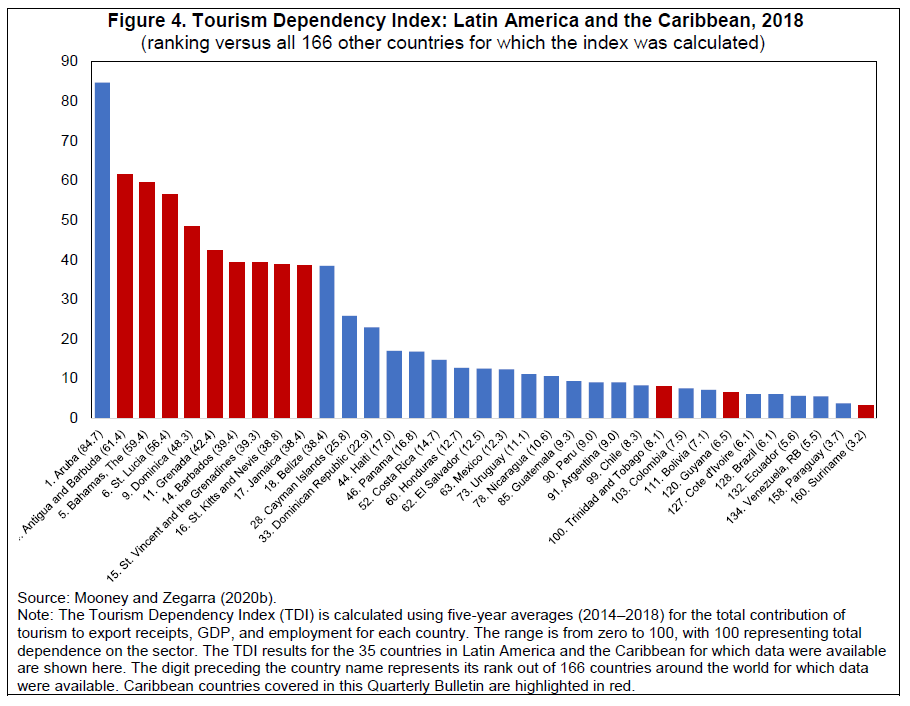

As highlighted in the country sections, nearly a dozen Caribbean countries—including the six Organization of Eastern Caribbean States (OECS) sovereign countries, as well as The Bahamas, Barbados, and Jamaica—rank in the top 20 on a new global index of economic dependence on the sector, dubbed the Tourism Dependency Index (TDI). The TDI is calculated for 166 countries worldwide for which data were available. It uses five-year averages (2014–2018) for the total contribution of tourism to export receipts, output, and employment for each country. The range is from zero to 100, with 100 representing total dependence on the sector. Index results for 35 countries in Latin America and the Caribbean for which data were available are shown in Figure 4, with the countries analyzed in this Quarterly Bulletin highlighted in red.

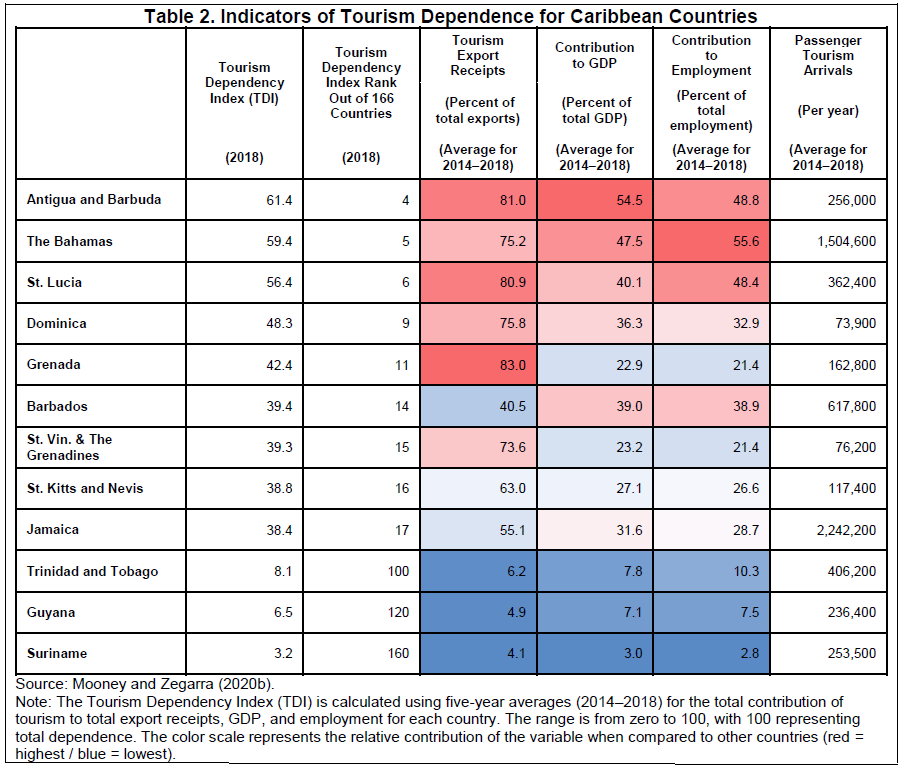

More specifically, the Caribbean countries covered in this Quarterly Bulletin are among the world’s most dependent on tourism with respect to the three critical variables included in the TDI index. For example, over three-quarters of export receipts are linked to tourism in Antigua and Barbuda, The Bahamas, Dominica, and Grenada (Table 2). Similarly, the total contribution of tourism is 40 percent or more in terms of both GDP and employment for Antigua and Barbuda, The Bahamas, St. Lucia, and Barbados. Taken together, this suggests that the Caribbean could be the most adversely affected region in the world in terms of the economic impact of COVID-19.

COVID-19 and the Shock to Tourism Flows: An Extreme Outlier

Given the importance of the tourism sector for the Caribbean countries, envisioning the impact of the crisis for tourism-dependent economies requires developing plausible scenarios for the removal of travel restrictions across source and destination countries, as well as the degree to which demand might rebound. In this context, a reasonable starting point is a review of historical tourism flows and the implications of past shocks for tourism arrivals to the region.

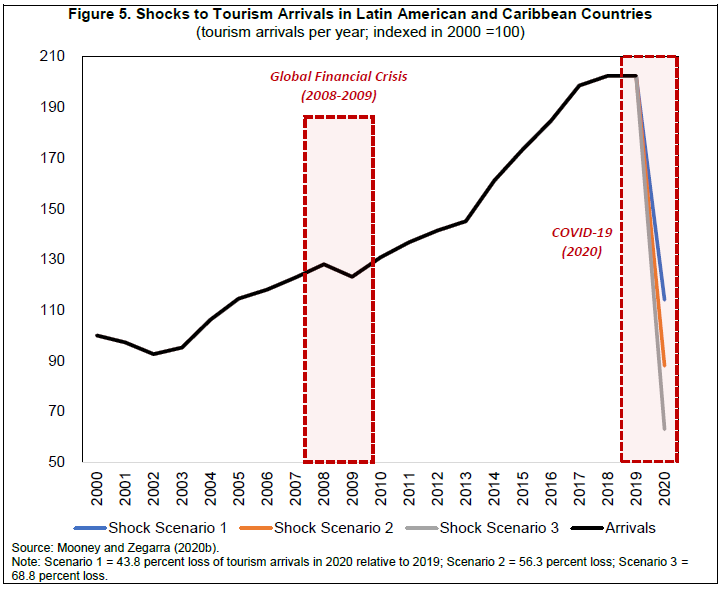

A review of tourism arrivals to LAC between 2000 and 2018 reveals that the largest single-year reduction was about 5 percent relative to the previous year in 2002. A similarly large reduction in tourism arrivals to the region was recorded following the global financial crisis of 2008–2009. In contrast, the near-complete shutdown of both passenger air travel and cruise ship activity beginning in March 2020 would imply a much larger shock to tourism arrivals and related receipts for 2020, and perhaps beyond.

Using available data on the evolution of flows to date and announced policies (including those discussed above), this section develops shock scenarios for tourism reflecting the complete dissipation of activity during the second quarter of 2020, and plausible paths for the sector’s recovery later in the year (Figure 5). These scenarios—which are very much in line with views expressed by experts representing the sector10—suggest that the shock to flows could be in the range of between 40 and 70 percent, making the implications of the COVID-19 crisis for Caribbean tourism an extreme outlier when compared to available historical data.11

Shock Simulations: Employment

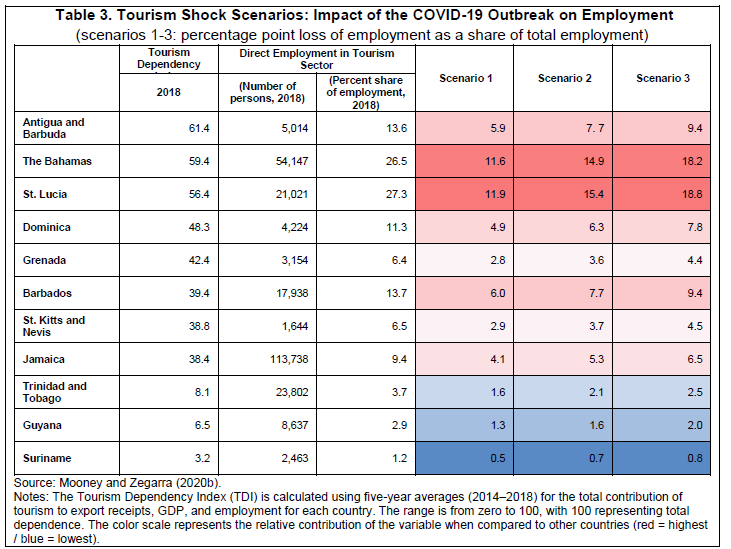

While results of similar shock simulations applied to economic output were included in the previous Quarterly Bulletin and an accompanying blog post (Mooney and Zegarra 2020a), Table 3 highlights the results of new simulations using the shock scenarios defined in Figure 5 to illustrate the potential implications of COVID-19 for employment across the region. For Caribbean countries that are most dependent on tourism, such as The Bahamas and St. Lucia, anywhere from 12 percent (Scenario 1) to as much as 20 percent of the labor force (Scenario 3) could be adversely affected by the pandemic. It is worth noting that these shocks have been applied to the direct contribution of the tourism industry to employment, which does not take into account other sectors (e.g., retail, services, construction) that are likely to be adversely affected by the loss of jobs and purchasing power for those working directly in tourism. Taken together, these and related exercises underscore the human dimensions of this crisis—many individuals and households in the region will suffer, implying severe social costs that are difficult to capture with economic aggregates. New data developed by the IDB on related issues are discussed later in this section.

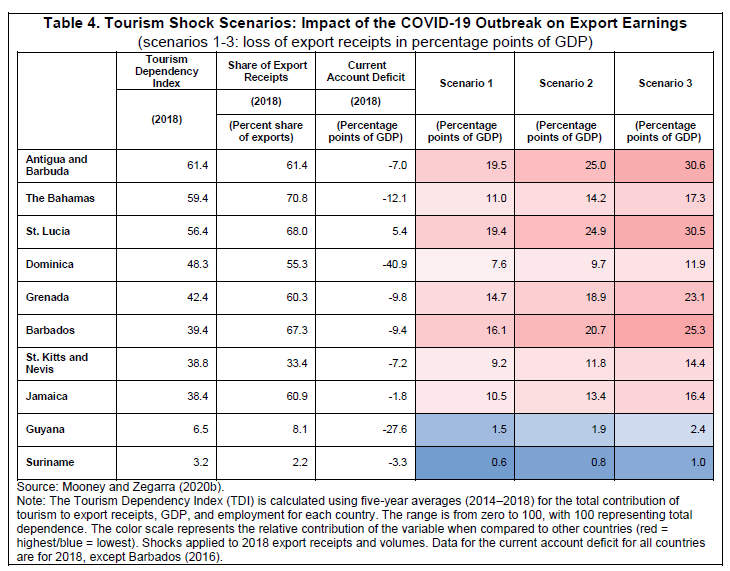

Shock Simulations: The Balance of Payments

Using the same three shock scenarios from Figure 5 applied to employment, Table 4 illustrates the potential implications of COVID-19 for export receipts and the current account. This is only a partial simulation, as the import content of tourism could be significant, meaning that simulations are likely to overestimate the shock to net exports. That said, the magnitudes of these simulated shocks are quite significant, with highly tourism-dependent countries potentially facing substantial losses of export receipts that, even under the least severe scenarios, are often much larger in magnitude than historical current account balances.

As no country can sustain a significant increase of the current account deficit without obtaining additional financing from abroad, shocks of this magnitude are likely to imply the need for adjustment in terms of the volume of imports. For this reason, and given the automatic adjustment in imports that a loss of tourism would imply (e.g., goods consumed locally by tourists),12 this analysis does not mean to suggest that current account deficits would widen by, for example, more than 25 percentage points of GDP, as in the case of Antigua and Barbuda, Barbados, or St. Lucia (depending on the shock applied). But what is clear from this exercise is that the crisis will force many tourism-dependent countries to undergo significant adjustments in terms of their commercial and financial transactions and relationships with international partners. Similarly, there could be unprecedented pressures on exchange rates and financing flows, requiring difficult decisions by both public and private sectors.

So far, Jamaica’s floating exchange rate has not experienced a large depreciation, and the other countries have either de facto or de jure fixed exchange rates. One summary indicator of balance of payments pressures has also fared quite well: the level of international reserves. The Bank of Jamaica reports that gross reserves have increased since the end of February and, netting out the use of IMF resources (the May disbursement under the Rapid Financing Instrument), reserves have shrunk by only about 5 percent since March. In The Bahamas, the Central Bank reports that reserves rose slightly from the end of February to the end of June, according to the Central Bank. The IMF (2020a) reports that net international reserves in Barbados increased between the end of 2019 and April 2020, buoyed by disbursements from international financial institutions. In Guyana, net international reserves have fallen slightly (3 percent) since February but were on a rising trend through May, according to the Central Bank. For Trinidad and Tobago, the Central Bank reports that net international reserves fell in March, but they were back up to February levels in May. In Suriname, black market premia for the exchange rate have soared as severe foreign exchange shortages persist.

V. Social Impact of the Crisis

Lockdown measures have made it difficult to conduct traditional face-to-face household surveys to monitor the social situation across Latin America and the Caribbean. The IDB’s Research Department launched an online platform to collect information on social conditions in the middle of the crisis, but this approach is not the same as collecting data from a representative sample. That said, for the Caribbean countries, the IDB’s Caribbean economics team joined forces with the Research Department to reweight the data collected online using information from representative household-level surveys across Caribbean countries.13 The empirical results, therefore, are already calibrated to meet representative socioeconomic parameters of Caribbean populations. The findings were presented in a blog post in May by Beuermann et al. (2020) and are reproduced here.

The survey was conducted from April 16–30, and about 12,500 households responded.14 One striking feature is the nutritional impact of the crisis. For households earning less than the minimum wage, a striking 34.3 percent of respondents declared that they had gone hungry in the previous week, and just over half stated that they consumed less healthy food (Figure 6). These issues even persist, at substantially lower levels, in the higher-income categories.

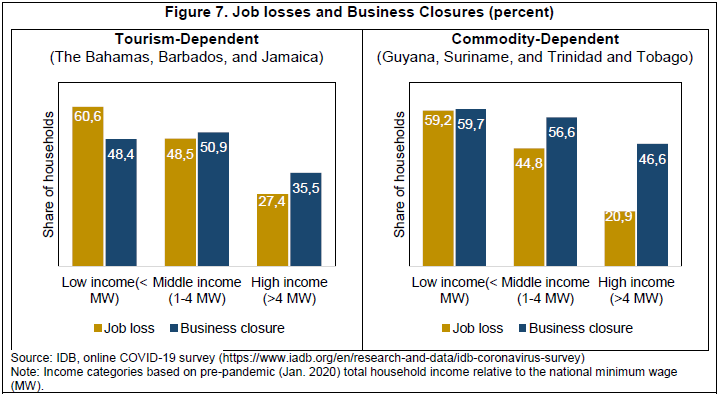

Labor market outcomes have also been dramatic, with job losses and business closures for business owners reported at a high level in both tourism- and commodity-dependent economies (Figure 7). The numbers are worse for the poor, the households that generally have the smallest savings buffers.

There are also important gender dimensions revealed by the survey. According to the responses, outcomes have been worse for female-headed households than for male-headed households. As shown in Figure 8, job losses and nutritional outcomes are two examples, and the gaps are large. In addition, some women have reported an increase in domestic violence.

VI. Imagining the Future15

The previous sections provide an overview of ongoing developments in the Caribbean. With coronavirus curves flattened and airports opening, the region can begin to think of a transition to a post-crisis scenario. The pace and success of the transition obviously will depend on external developments, given that these are very small, open economies. First, these countries depend on imports for testing, protective equipment, and, eventually, a vaccine—if and when one is developed. Second, the ability to sustain social distancing measures and finance social support programs for families and firms will depend on the potential for recovery of key sectors: tourism in three countries, and commodities in the other three. The performance of both sectors will depend on the evolution of the global economy, as well as structural security protocols for tourism that could facilitate a recovery in international travel. Third, other countries’ efforts to control the virus will also affect prospects for international tourism, and the ability of those countries to remove social distancing programs could then support a rise in oil and gas prices. In brief, the transition towards recovery for the Caribbean itself will depend on external events.

Pressures on the macro framework could complicate the transition. Jamaica has a floating exchange rate regime, supported by an explicit inflation-targeting monetary policy framework. If devaluation is limited, this could support a balance of payments adjustment, without fueling excessive inflation, and could also improve competitiveness for the future recovery. The other countries in the Caribbean have either de jure or de facto fixed exchange rates. The fiscal policy framework varies across the six countries covered here. Some countries have relatively stronger medium-term fiscal frameworks, which could help ease market concerns when deficits inevitably expand due to the fiscal cost of measures to combat the social and economic cost of the crisis. External finance from multilaterals can close financing gaps and relieve short-term liquidity concerns.

Social pressures and electoral processes could complicate the transition. Five of the six countries analyzed here are experiencing a sharp economic contraction and sharp increases in unemployment.16 Depending on the testing and health sector capacity mentioned above, the transition measures will have to be gradual, and there could be setbacks. There is a high degree of uncertainty on both the scientific and economic fronts. Social tensions may mount. Problems such as increased domestic violence and child abuse are a concern, as are already high and rising suicide rates, by international standards. Female employment conditions in service sectors—so-called “care” sectors—could suffer disproportionately. Food insecurity is another threat, driven either by supply chain disruptions or a lack of foreign currency. Finally, as noted above, four of the six countries—Guyana, Jamaica, Suriname, and Trinidad and Tobago—either already had elections or will have one within the next 12 months. There will be electoral transitions in the middle of the COVID-19 transition, and this could generate uncertainty about the policy path from transition to recovery. It also creates an opportunity for reinvigorated consensus for new policy reforms.

For the small, open economies of the Caribbean, the path for recovery also depends on external developments. The recovery of the tourism sector will depend on international cooperation on travel rules and sanitary protocols, as well as on economic conditions in source countries—particularly the United States, Canada, and Europe. Clearly, commodity prices will evolve according to international market developments. Even the gold price could drop somewhat if international financial markets return to long-term stability and gold’s safe-haven allure fades. Oil and natural gas prices could strengthen if workers return to their normal commute patterns, but perhaps that will not happen. The possible reconfiguration of global supply chains could open, or close, opportunities for foreign direct investment in business process outsourcing and other global services. In brief, there are multiple external factors that pose opportunities and risks for a recovery of Caribbean economies.

The recovery will also depend on the success of the crisis response and domestic transition policies. The recovery will be built on the efforts of households, businesses, and governments. Emerging from the transition stage, if many households and/or firms are bankrupt and if people are still getting sick, then the recovery is likely to be prolonged and slow. The risk of imported cases looms large as international travelers begin to arrive.

One domestic factor that will need to be addressed is to recover fiscal sustainability following a buildup in public debt. Deficit spending in response to the crisis will result in an increase in debt. Three key areas will be essential for management of that debt:

-

Improve expenditure efficiency and effectiveness. Detailed public expenditure reviews and sector analysis will be key for getting the most out of ever more limited fiscal space. Recommendations from the IDB are outlined in an IDB blog that looks at fiscal policy during the coronavirus crisis (Izqueirdo and Ardanaz 2020).17

-

Improve debt management. More debt implies a greater need to minimize debt costs and smooth the payment profile. Institutional reforms to improve debt planning, analysis, investor communication, and other areas can help in that regard.

-

Attend to other longstanding institutional challenges in fiscal policy. Some countries are more advanced than others, but depending on the country, areas for improvement include medium-term expenditure frameworks, fiscal rules, heritage funds (for natural resource exporters), stabilization funds, and the incorporation of disaster risk concerns into the fiscal framework.

The recovery may benefit from lessons learned from the crisis, particularly in terms of new dimensions of resilience. Business continuity is an obvious lesson for both the public and private sectors. This puts a premium on some traditional areas as well as new areas for policy reform and investment. The following actions could also broaden the opportunities for new sectors of investment:

-

Strengthen health emergency capacity. There may be another surge of the virus or more novel viruses in the future.

-

Strengthen social safety nets. Some countries have stronger systems than others, but the distributional bias in terms of the impact of crisis implies the need for improvement.

-

Develop Internet connectivity for all. This may require some public investment and regulatory redesign and rethinking. Infrastructure for both cable and wireless communication can be improved. Social tariffs of some form may be necessary to improve access for poorer households and smaller firms.

-

Increase digital government and reduce tape. This is a long-standing issue, and some governments have progressed more than others. Social distancing has been a wake-up call. While technology can facilitate governance, the processes and procedures themselves have to simplified, and that requires legal and institutional reforms. Small Caribbean countries could copy Estonia—which has been a leader in this area among small countries--and reach the frontier.

-

Improve data. This is related to the digital government theme, but a separate set of actions and reforms are needed to finally make better use of existing administrative data, link to survey data, connect to digital records, institute digital IDs, etc.

-

Strengthen private sector resilience. From a management perspective, the government can work with business leaders to think through how they can temporarily convert human and physical capital into new activities when an existential crisis arrives. More data and analysis of management practices and skills in Caribbean countries would also be useful.

-

“Go regional” on food and some other supply chains. Given the small size of Caribbean economies, going regional on basic essential items such as foodstuffs and medical supplies and equipment could open new economic opportunities and enhance economic resilience. There is scope for some of the countries to become important regional sources of food. Regional procurement, storage, and even technological development of medical supplies and equipment would also enhance resilience.

Addressing longstanding challenges could also help enhance the recovery. Many traditional challenges remain relevant, and these have been analyzed in the IDB’s Country Development Challenges documents. The details are country-specific, but several broad themes are:

-

Getting the most out of traditional lead sectors. The idea here would be to build domestic supply chains to get value-added linkages from tourism in some countries and from natural resources in others. An obvious area would be agriculture for foodstuffs for the hospitality and restaurant sectors. Eco-tourism drawing on natural resources of tropical forests has large potential in Guyana and Suriname. Those two countries could also expand sustainable forestry and agricultural exports. Another potential growth area is in “business continuity” tourism. If there is an increasing trend to working remotely, then pleasant tourist destinations could host those workers. Barbados is preparing a 12-month “Barbados Welcome Stamp” precisely to facilitate this type of service.

-

Quality education for everyone. The education sector continues to lag and to constrain global service possibilities in Caribbean countries. It also limits the capacity for innovation. Differences in quality between schools and between social classes also constrain the ability to develop technology clusters.

-

Climate change/Green recovery. Hurricanes are expected to only get worse in the years ahead, and sea-level rise is a major threat for all of the Caribbean countries. Eventually, economies will have no choice but to diversify away from hydrocarbons.

Governments across the globe have been improvising, experimenting, and struggling to implement their responses to the novel coronavirus crisis. The Caribbean countries discussed here are no exception. Although these countries have been leaders in “flattening the curve,” they will be strongly impacted as the world moves forward to the transition and recovery phases. There will be continued uncertainty about the characteristics of the virus itself, including the strength and duration of the immunity enjoyed by recovered patients. Strengthening the capacity for testing, contract tracing, and treatment is still needed, even as curves may have been at least temporarily flattened in most of these countries.

Selected References

Beuermann, Diether W., Laura Giles Álvarez, Bridget Hoffmann, and Diego Vera-Cossio. 2020. “COVID-19, The Caribbean Crisis.” Caribbean DevTrends, May 14. Available at: https://blogs.iadb.org/caribbean-dev-trends/en/covid-19-the-caribbean-crisis/

Caribbean Country Department. 2020. “LAC Post COVID-19: Challenges and Opportunities.” Inter-American Development Bank, Washington, DC. Available at: https://publications.iadb.org/publications/english/document/LAC-Post-COVID-19-Challenges-and-Opportunities-for-CCB.pdf

Hale, Thomas, Sam Webster, Anna Petherick, Toby Phillips, and Beatriz Kira. 2020 “Oxford COVID-19 Government Response Tracker.” Blavatnik School of Government, University of Oxford, United Kingdom.

International Monetary Fund (IMF). 2019. World Economic Outlook. Washington, DC: IMF, October.

International Monetary Fund (IMF). 2020a. World Economic Outlook. Washington, DC: IMF, April.

International Monetary Fund (IMF). 2020b. “Request for Purchase under the Rapid Financing Instrument.” IMF Country Report 20/191. IMF, Washington, DC.

International Monetary Fund (IMF). 2020c. “Barbados: Third Review under the Extended Arrangement.” IMF Country Report 20/192. IMF, Washington, DC.

Izquierdo, Alejandro, and Martin Ardanaz. 2020. “Fiscal Policy in the Time of the Coronavirus: Constraints and Policy Options for Latin American and Caribbean Countries.” Ideas Matter, March 31. Available at: https://blogs.iadb.org/ideas-matter/en/fiscal-policy-in-the-time-of-coronavirus-constraints-and-policy-options-for-latin-american-and-caribbean-countries/

Izquierdo, Alejandro, Carola Pessino, and Guillermo Vuletin (editors). 2018. Development in the Americas: Better Spending for Better Lives. Washington, DC. Inter-American Development Bank. Available at: https://flagships.iadb.org/en/DIA2018/Better-Spending-for-Better-Lives

Mooney, Henry, and María Alejandra Zegarra. 2020a. “COVID-19: Tourism-Based Shock Scenarios for Caribbean Countries.” Caribbean DevTrends, March 16. Available at: https://blogs.iadb.org/caribbean-dev-trends/en/covid-19-tourism-based-shock-scenarios-for-caribbean-countries/

Mooney, Henry, and María Alejandra Zegarra. 2020b. “Extreme Outlier: The Pandemic’s Unprecedented Shock to Tourism in Latin America and the Caribbean.” IDB Policy Brief 339. Inter-American Development Bank, Washington, DC. Available at https://publications.iadb.org/en/extreme-outlier-the-pandemics-unprecedented-shock-to-tourism-in-latin-america-and-the-caribbean

Mooney, Henry, and María Alejandra Zegarra. 2020c. “The Pandemic’s Unprecedented Shock to Tourism in Latin America and the Caribbean.”, in “COVID-19 in Developing Economies.” edited by Simeon Djankov and Ugo Panizza. Center for Economic Policy Research, London, United Kingdom. Available at: https://voxeu.org/content/covid-19-developing-economies

Mooney, Henry, Allan Wright, and Kari Grenade. 2018. “Fiscal Councils: Evidence, Common Features and Lessons for the Caribbean.” IDB Policy Brief No. 300. Inter-American Development Bank, Washington DC. Available at: https://publications.iadb.org/en/fiscal-councils-evidence-common-features-and-lessons-caribbean

World Travel and Tourism Council. 2004. “The Caribbean: The Impact of Travel and Tourism on Jobs and the Economy.” Available at: http://www.caribbeanhotelandtourism.com/downloads/Pubs_WTTCReport.pdf

[1] The Caribbean region refers to the six member countries of the Inter-American Development Bank that correspond to its Caribbean Country Department: The Bahamas, Barbados, Guyana, Jamaica, Suriname, and Trinidad and Tobago.

[2] The survey is available at https://www.iadb.org/en/research-and-data/idb-coronavirus-survey

[3] OECS countries covered by the IDB’s Caribbean Department are Antigua and Barbuda, Dominica, Grenada, St. Lucia, St. Vincent and the Grenadines, and St. Kitts and Nevis.

[4] The states of the Amazon region in Brazil have the highest level of per capita coronavirus infections in that country.

[5] The Bahamas is not included in the index, but that country has also undertaken strong measures.

[6] Short-term oversupply even led to negative WTI prices for delivery this spring. Brent prices have been less volatile in recent months and have stabilized at just over US$40 per barrel.

[7] According to the World Bank’s Commodity Markets Outlook, April 2020.

[8] The UN World Tourism Organization estimates that global tourism flows fell by over 20 percent in the first quarter of 2020. See https://www.unwto.org/news/covid-19-international-tourist-numbers-could-fall-60-80-in-2020.

[9] The paper also develops an original index of tourism dependency and evaluates the economic and employment impacts of multiple tourism shock scenarios.

[10] For example, the UN World Tourism Organization estimated a 97 percent drop in international tourist arrivals relative to previous years for April 2020 (https://www.unwto.org/es/news/los-nuevos-datos-muestran-el-impacto-de-covid-19-en-el-turismo).

[11] In statistics, extreme outliers are usually described as outcomes that lie more than three standard deviations from the mean for a normally distributed population.

[12] The World Travel and Tourism Council (2004) estimated that imports represent one-third of the total (direct and indirect) contribution to GDP and are actually larger than the direct contribution. See page 32 of: http://www.caribbeanhotelandtourism.com/downloads/Pubs_WTTCReport.pdf

[13] The aggregates presented here are for the six Caribbean countries covered in this Quarterly Bulletin.

[14] The survey is available at https://www.iadb.org/en/research-and-data/idb-coronavirus-survey

[15] The section draws on a policy brief by the IDB Caribbean Country Department (2020).

[16] Guyana’s oil production boom will still result in positive growth, despite the decline in oil prices.

[17] The blog draws on more detailed analysis from the IDB flagship report entitled Better Spending for Better Lives (Izquierdo, Pessino, and Vuletin, 2020).

David Rosenblatt

David Rosenblatt is the Regional Economic Adviser for the Caribbean Country Department at the Inter-American Development Bank (IDB).

Henry Mooney

Henry Mooney serves as Economics Advisor with the IDB’s Caribbean Department, and was formerly the Bank's Lead Economist based in Jamaica.