“Relatively low numbers of cases in Jamaica are linked to early and decisive action on the part of the government to contain the virus. Jamaica’s success with fiscal and economic reform in recent years put it in a strong position to face the crisis, but the country’s extreme dependence on tourism and external demand mean that the economic and social impacts will be severe.”

Update on COVID Outbreak

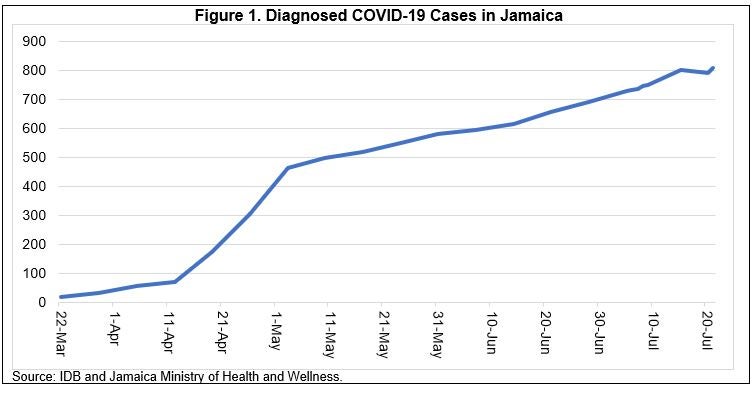

On March 10, Jamaica recorded its first case of the coronavirus, which prompted authorities to initiate a number of measures aimed at stopping the spread of the virus. Cases rose quickly to approximately 100 during the first 30 days1 (through April 10), with many of these initial cases linked to a localized outbreak at a single enterprise. As of July 20, there were approximately 800 cases of the virus identified on the island (Figure 1), based on about 22,000 administered tests. Of these, 10 fatalities were attributed to the crisis.

Prevention and Response Measures

Relatively low numbers of cases in Jamaica are undoubtedly linked to early and decisive action on the part of the government to contain the virus. These measures include border and travel restrictions, mandatory quarantines, public information campaigns, as well as public health measures aimed at improving the system’s capacity to test and deal with infections. In particular, authorities declared a national emergency, which provided the government with legal and other authorities required to limit business operations and other activities where people might gather (e.g., schools, places of worship, etc.), and to impose sanctions for non-compliance. A nationwide curfew followed in an effort to further curtail social gathering, as well as localized lockdowns when cases began to increase in certain areas.

More recently, with a slowing of the rate of transmission, authorities have begun the process of reopening. The first phase of reopening began with churches and bars on May 19, followed by the lifting of stay at home orders on June 1, as well as the restart of in-class sessions for senior secondary students on June 8. More recently, air and sea ports were allowed to reopen to international travel on June 15, with the tourism sector slated to begin accepting bookings, depending on demand. Inbound passengers from abroad will be subject to special procedures, including that all passengers require travel authorization that must be sought prior to arrival. Upon arrival, all travelers will undergo a short risk assessment by a public health officer. If officers identify a high risk—e.g., symptoms of COVID-19, or if a passenger has traveled from or through countries where there is high community transmission of COVID-19—, individuals would be subject to a PCR test2, and be placed in quarantine for up to 48 hours until results are available. If tests prove negative, travelers would be allowed to move within Jamaica's “COVID-19 Resilient Corridor”3, while following all hygiene measures that are in place. If tests are positive, the traveler would be placed in isolation. Additional restrictions were also imposed in July for travelers from high-risk locations, including New York, Florida, Arizona and Texas, who are required to upload a negative COVID-19 PCR test result 10 days prior to arrival in order to obtain approval to travel to Jamaica.

Economic Context and Shock

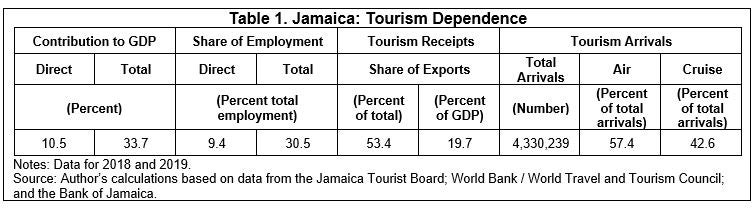

COVID-19 implies a significant shock to Jamaica, particularly given its dependence on tourism. As detailed in our introductory section and Table 1 (below), Jamaica is one of the most tourism-dependent economies in the world, relying crucially on the sector for export receipts, employment, and output. In this context, the total contribution of tourism to employment and output is about 30 percent, while tourism receipts are the equivalent of about 50 percent of all export revenues. While as detailed above, ports of entry have reopened to travelers from abroad, stringent restrictions on outbound and return travel in key source countries (e.g., the United States, Canada, Europe) continue to stifle the tourism industry. Similarly, both the attitudes of would-be travelers, and the impacts of the crisis on disposable incomes may continue to create hurdles for the sector over the coming months and into next year.

Given many lingering uncertainties, it is difficult to estimate the impact on economic performance with any degree of precision. After successfully graduating from long-term IMF support in November 2019, the Government of Jamaica requested emergency assistance from the IMF under the Rapid Financing Instrument (RFI) in March of 2020. This assistance—equal to about US$520 million dollars—has not been allocated to fiscal financing requirements, but will instead be used to reinforce external buffers of the central bank. The most recent projection from the IMF and GOJ (May 2020) envisions a GDP declaration of -5.3 percent in FY2020/214, and a strong rebound the following year. While the prospects for a return to pre-crisis levels of tourism remain uncertain, the nature of the shock is such that we would expect a strong recovery once the sector resumes operation—the IMF’s current estimates for FY2021/22 are for real GDP growth of about 3.9 percent.

In this context, the GOJ’s successful economic reform effort from 2013 to 2019 put the country in a relatively strong position to confront this unprecedent shock. Notable achievements since 2013 include a reduction of the public debt-to-GDP ratio from 146 percent to 94 percent (at end-FY2019/20); a shift from managed to floating exchange rates; implementation of a functioning inflation targeting framework in 2017; and, a strong improvement of external buffers. Against this backdrop, the GOJ entered the crisis from a position of strength at end March 2020, including: strong reserves buffers (~24 weeks of imports); a large reprogrammable fiscal envelope (i.e., both primary and overall balance surpluses); and, a strong cash position originally earmarked for debt repayment (equal to about 4 percent of GDP). As a result, the recent supplemental budget outlining crisis response measures and updated fiscal projections envisions lower gross domestic and external financing requirements than expected prior to the crisis, owing to the reorientation of funds for debt repayment to financing needs for FY2020/21. As noted earlier, the IMF RFI resources are not being used for government financing, and are meant to serve as supplemental external buffers. Against this backdrop, the exchange rate has remained broadly stable, and the Bank of Jamaica (BOJ) has refrained from large or sustained intervention in the foreign exchange market.

The GOJ has undertaken a number of measures to address the crisis, including as outlined in a supplemental budget released in May. In the supplemental budget, the GOJ announced tax cuts equal to about 0.6 percent of GDP, along with targeted expenditure measures equal to about 0.5 percent of GDP in stimulus to counteract the effects of COVID-19. Tax cuts include a reduction in the standard GCT rate from 16.5 to 15.0 percent, and an income tax credit for companies with annual sales/revenue less than or equal to J$500 million. On the expenditure side, significant measures include a program dubbed “COVID-19 Allocation of Resources for Employees” (CARE), which provides cash transfers to businesses in targeted sectors based on the number of workers employed; transfers to individuals who have lost employment since March; as well as grants targeted to the most vulnerable segments of society. Additional measures have been announced to support the most affected sectors, including customs duty waivers on medical supplies and sanitizers and a cash transfer program for businesses in targeted sectors and individuals who lost employment.

While the crisis does imply adjustment, expectations are that the primary balance will remain in surplus, and that financing needs will be limited. As budgetary objectives are linked to the Fiscal Responsibility Law’s (FRL) medium-term debt targets, the delay of the debt target has allowed the government to accommodate the impact of the crisis by reducing the overall and primary balance targets for FY2020/21 from 0.4 percent of GDP and 6.5 percent of GDP, to -2.9 percent of GDP and 3.5 percent of GDP, respectively (table below). Expectations are that the primary surplus target would be increased to 5.4 percent of GDP next fiscal year, barring a further deterioration in outcomes. This will imply a larger gross financing need for FY2020/21—increasing from an originally estimated 8.6 percent of GDP to 12.0 percent of GDP. Despite the increased funding requirement of about 3.6 percentage points of GDP, both domestic and external financing needs are programed to fall relative to pre-crisis expectations, as the government has shifted about 4.2 percentage points of GDP in cash deposits from planned debt reduction to fiscal financing. Note that the IMF RFI disbursement—equal to about 3.4 percent of GDP—has not been allocated to government financing, but the Fund has approved it for budget support, should the GOJ have larger than expected funding requirements.

Looking forward, durable fiscal institutional reforms undertaken in recent years should help guide post-crisis policies and safeguard long-term sustainability. Related reforms include the development and implementation of the FRL in 2014, with quantitative targets for budgetary outcomes and debt reduction (e.g., a debt to GDP ratio of <60 percent), as well as broader improvements in processes, capacity, and legislation. This debt target has now been pushed back from 2026 to 2028 owing to the crisis, taking advantage of escape clauses built into the FRL. Should outcomes deteriorate, the framework would allow for further flexibility. Authorities have also made progress with other institutional reforms aimed at enhancing prudence, including efforts to develop an independent fiscal council, as well as reforms of the central bank that will increase its independence and insulate it from possible pressure to finance the government in future.

Despite the shock to tourism exports, the exchange rate has remained broadly stable, and the BOJ’s reserves remain ample. The Minister of Finance approved a continuous medium-term inflation target band of between 4 percent and 6 percent for the Bank of Jamaica in September 2017. This shift in policy has helped to improve the transparency, predictability, and effectiveness of monetary policy, with positive implications for market conditions and expectations. Despite the shock to export receipts, the Jamaican dollar has remained broadly stable versus the US dollar and other currencies, and the BOJ has refrained from large scale intervention, leaving its reserves broadly intact. In this context, net international reserves stood at an estimated 38 weeks of next year’s goods and services imports at end-May 2020 (latest available). Note that the IMF RFI disbursement—equal to US$ 520 million—is also currently being used to supplement the BOJ’s externa buffers. The current account is expected to deteriorate in the near term, but recover once the shock dissipates. The shock to tourism exports will imply a deterioration of the current account over the near term, though this deterioration will be dampened by the fact that: (i) tourism also generates considerable import demand, and (ii) oil prices and demand for fuel have fallen. At present, the expectation is that the current account will deteriorate to about -7.3 percent of GDP in FY2020/21 and -4.3 percent the following year.

Jamaica’s financial sector entered the crisis with strong capital buffers and stability indicators. Prior to the crisis, banks had been enjoying unprecedently strong domestic conditions. They had been able to build ample capital buffers (relative to regulatory requirements); displayed strong balance sheets and asset quality (e.g., low levels of non-performing loans); and, both policy and market-determined interest rates had fallen to record lows, which coupled with declining domestic government financing requirements (from debt reduction) meant that the sector had ample liquidity. The crisis will undoubtedly affect asset quality given the large share of the economy exposed to the tourism sector, but we expect that a combination of strong initial conditions and supplemental measures taken by the central bank to support liquidity (e.g., making emergency liquidity facilities more easily available, lower reserve requirements, etc.) will help avoid a pronounced or systemic crisis.

Social Sector

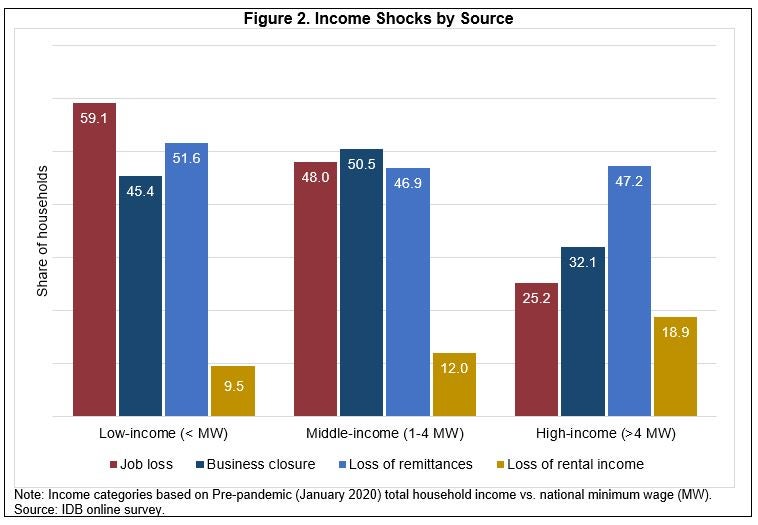

The Inter-American Development Bank conducted an online survey during the second half of April. The responses from the survey for Jamaica were sobering. Nearly 60 percent of low-income households (earning less than the minimum wage) reported a job loss in the household, and even a quarter of higher income families reported a job loss as well. There was a reported decline in remittances for over half of low-income families, and nearly half of families in other income categories. Business closures have also been reportedly high across low and middle-income households. While not meeting the statistical standards of a full household survey, this online survey does provide important evidence of the extent of the social impact during the height of the lockdown.

1 Ministry of Health and Wellness - https://jamcovid19.moh.gov.jm/

2 Polymerise chain reaction (PCR) and antibody testing for Covid-19.

3 The “COVID-19 Resilient Corridor” is a defined geographical area within Jamaica designated for tourism purposes.

4 The fiscal year begins on April 1.

Henry Mooney

Henry Mooney serves as Economics Advisor with the IDB’s Caribbean Department, and was formerly the Bank's Lead Economist based in Jamaica.

Jason Christie

Jason Christie is an economist with the Inter-American Development Bank’s Caribbean Country Department in Jamaica, where he focuses on economic research and operations, including related to strategy development and programming for IDB lending and related activities.