Due to the recent spike in Covid-19 cases, the authorities strengthened social distancing measures and lockdowns.

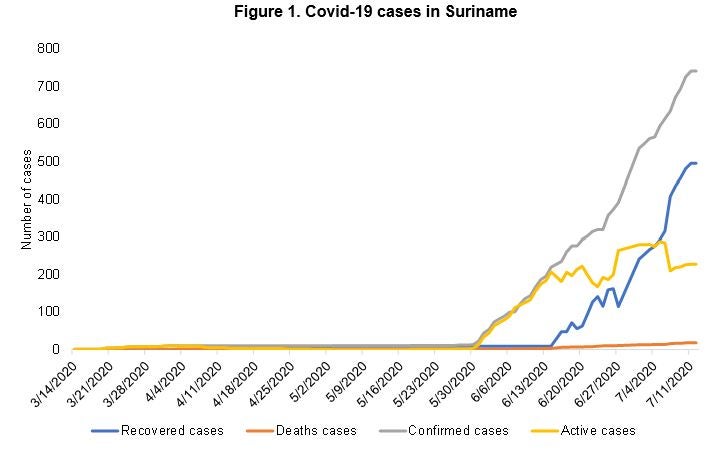

Suriname confirmed its first imported Covid-19 case on March 13, 2020. As of July 12, the authorities confirmed a total of 741 cases, active cases are currently at 228 with 18 COVID-19 related deaths, 495 recovered, and 166 persons in quarantine. Suriname, although flattening the curve and reporting a short period (roughly two weeks) of no active Covid-19 cases, is now along a path of exponential growth in Covid-19 cases (Figure 1).1 The rate of Covid-19 tests performed is improving, currently a total of 1,244 tests performed (or 2,120 tests per million population) but remains lower that it’s regional counterparts: Guyana’s (4,134 tests per million population), 9,528 tests per million for Jamaica, 4,147 tests per million for Trinidad and Tobago and 30,739 tests per million for Barbados.2

Due to the recent spike in Covid-19 cases, the authorities strengthened social distancing measures and lockdowns. On June 3, the government announced a total lockdown of the country from June 8 for a period of two weeks. The specific measures include: (i) restrictions on leaving home; (ii) public gatherings are restricted to a maximum of 5 people; (iii) all non-essential companies are closed; (iv) the borders via land, water and air remain closed; and (v) private cars and taxis are allowed to have a maximum of 2 occupants. Meanwhile, the Ministry of Trade, Industry and Tourism has also provided strict guidelines for companies that are open. After June 21, some restrictions were relaxed while maintaining strict sanitary measures.

Economic Shock

Suriname is experiencing its second major shock within a six year period. The country’s economy went into a deep recession in 2015 following a sharp decline in the price of its main export commodities (gold and oil) and cessation of alumina production. The country’s economy has not recovered from the 2015 recession. As a consequence, Suriname is facing the ongoing COVID-19 pandemic with inadequate fiscal buffers, large twin deficits (fiscal and current account), low growth, high debt levels, low international reserves and a large disequilibrium in the foreign exchange market. Suriname was downgraded with a negative outlook by Fitch, Moody’s and Standard and Poor’s in the first half of 2020. Suriname also announced successful results of Consent Solicitation for a new repayment schedule relating to its 9.875 percent Notes due 2023.3

The ongoing COVID-19 shock would mostly impact economic growth through commodity prices and the partial lockdown of the domestic economy. Suriname’s economy is heavily dependent on mining and oil sectors which together accounts for about 20.6 percent of GDP. On one hand, crude oil prices have declined by almost 51 percent in the first quarter of 2020 and are expected to remain low for the rest of the year, negatively impacting growth. However, gold which accounts for a relatively large share of GDP (15 percent) will help to partially offset the decline as gold prices have increased by 14 percent over the same period. The service sectors (wholesale and retail, transportation, hotels and restaurants etc.) account for 49 percent of Suriname’s GDP. The service sectors are adversely affected by ongoing COVID-19 related lockdowns. Taking into account these shocks, the IMF is projecting that real GDP would contract by at least 5 percent in 2020.

Potential job and income losses are expected to be relatively large. Although data on job or income losses due to Covid-19 is not yet available, preliminary data from a recent online socioeconomic survey carried out by the Inter-American Development Bank shows a larger prevalence of job losses in households that earned below the minimum wage. Moreover, data from the 2017 Survey of Living Conditions shows that vulnerable sectors such as hotel and restaurants, retail, transportation, and construction account for more than 72 percent of permanent full-time private sector employee, implying that temporary job losses could be large (see Khadan, 2020).4

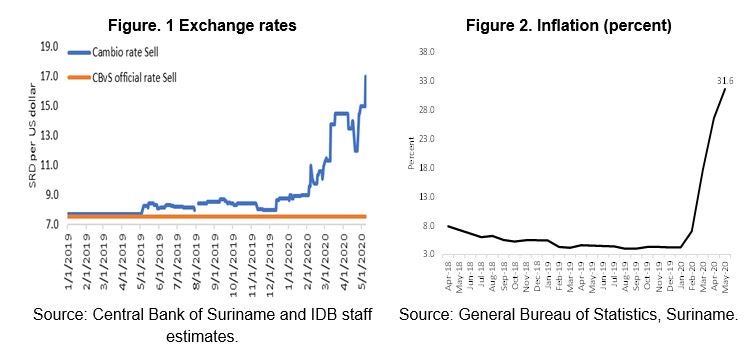

The parallel market exchange rate premium is contributing to higher inflation. There has been an acute shortage of dollars in the domestic economy in recent years. As a result, the parallel market exchange rate has been increasing since 2019. As of May 2020, the parallel market premium was estimated to be 125 percent. The inflation rate at the end of May 2020 inflation rate increased to 31.6 percent from 4.2 percent at the end of 2019 (year on year, Figure 2). There were noticeable increases in the sub-components related to transportation, alcoholic beverages and tobacco, and household furnishings. This is mostly related to the large parallel exchange rate market premium—firms are already increasing their prices to reflect the parallel market exchange rate.

Interest rates in local currency have remained relatively stable. The average deposit interest rate in SRD decreased from 9.1 percent in March 2019 to 8.6 percent in March 2020. The average lending rate increased to 14.9 percent from 15.2 percent over the same period. There were marginal changes in lending and deposit rates in U.S. dollars and Euros: the lending rate for US dollars slightly increased from 8.1 percent in March 2019 to 8.6 percent March 2020 while the deposit rate fell from 2.9 percent to 2.7 percent over the same period; the lending rate for Euro dollars increased from 8.2 percent in March 2019 to 8.4 percent in March 2020 and the deposit rate fell from 0.5 percent to 0.4 percent over the same period.

Private sector credit could improve on account of a more accommodative monetary stance. Private sector credit declined from 38.1 percent of GDP in 2016 to 24.3 percent of GDP in 2019. Data from the CBvS show that while credit to the private sector in local currency (SRD) increased by 18 percent in March 2020 (year on year), credit in U.S. dollars and Euros declined by 9.5 percent and 6.3 percent, respectively, over the same period. In May 2020, the CBvS temporarily lowered the local currency cash reserve requirement from 35 percent to 27.5 percent. This measure will enable commercial banks to provide new short-term loans to private sector companies and to individuals affected by the COVID-19 pandemic at a proposed interest rate of 7.5 percent, which is significantly lower than the current market interest rate. The CBvS is also discussing with commercial banks the feasibility of granting 3 to 6 months deferral of payments to companies and individuals who are affected by the COVID-19 pandemic.

External sector performance

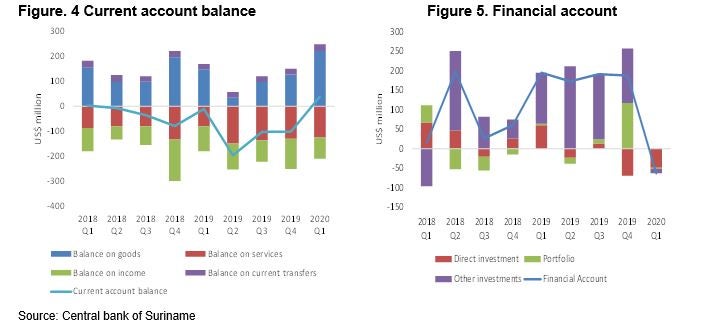

Preliminary data shows a marginal improvement in the current account balance in the first quarter of 2020. The current account balance slightly improved in the first quarter of 2020 to US$39 million from a deficit of US$10.7 million in 2019 Q1. The improvement in the current account balance in the first quarter was related to an improvement in goods exports, particularly mining: gold exports increased by 14 percent year on year compared to 2019 Q1. There was also marginal increase in non-mining exports, due mostly to rice exports and a 2 percent decline in imports for the same period. Foreign direct investment fell from a high of 9.6 percent of GDP in 2016 to 0.2 percent of GDP in 2019 and continued to decline in the first quarter of 2020 following the completion of the investments in the mining sector. The portfolio investment balance slightly worsened to US$˗3.4 million in 2020 Q1, from 4.3 million in 2019 Q1 (see Figures 4 and 5).

Social Sector

On the social response, the authorities established a SRD400 million Emergency Fund to finance social support measures including housing related expenses. A separate SRD300 million Production Fund was established to support small and medium-sized enterprises. The Emergency Funds will manage both national and international resources obtained for tackling the pandemic.5 Both funds will be financed by International Financial Institutions (IFIs) such as the World Bank, Inter-American Development Bank, Islamic Development Bank, Caribbean Development Bank and the domestic market. Social support measures for vulnerable groups have been announced for a period of six months. The government has increased the allowance for child support, old age provision, retirees (no previous government support), persons with disabilities, “weak households”, unemployment benefits for persons who have lost their income of jobs due to Covid-19 restrictions and social assistance benefits. The Emergency Fund will contribute approximately SRD 50 million to a Housing Fund. The target groups are those who do not have their own home or are not able to pay rent. A maximum of SRD 100,000 per loan can be provided with a grace period of 6 months.

1 This occurred after the country started to gradually lift social distancing restrictions in the lead up to the May 25 national elections.

2 See https://www.worldometers.info/coronavirus/

3 See https://www.bourse.lu/issuer/Suriname/83360

4 See https://publications.iadb.org/en/covid-19-socioeconomic-implications-on-suriname

5 See http://www.dna.sr/nieuws/wet-uitzonderingstoestand-covid-19-goedgekeurd/

Jeetendra Khadan

Jeetendra Khadan is a Senior Economist who holds the position of Country Economist for Suriname within the Caribbean Country Department at the Inter-American Development Bank.